Table of Contents

Today, we’ll go into the specifics of Amanah Saham and ASB financing.

Who’s this for?

How do I invest in this?

This will be the start of a series where we dive a bit deeper into each individual investment vehicle in Malaysia.

A list that we’ve roughly come up with:

- Amanah Saham

- Robo-advisors (Stash Away, MyTheo, Wahed)

- Funding Societies

- Fixed deposits

- Direct investment in the market

- Luno

Let’s start cornerstone of Malaysian investment, Amanah Saham!

Amanah Saham

Amanah Saham is a Malaysian investment fund managed by PNB.

The funds compromise of Malaysian stocks (think the likes of Maybank, Digi, Sime Darby) and fixed income assets.

We only recommend their fixed priced assets (ASB/ASM).

The reason for this is you get a nice amount of exposure to the Malaysian stock market, while safely knowing that your investment will not decrease in value.

Yeah, you heard that right.

You cannot lose money investing in ASB or ASM (unless they go bankrupt, which is extremely unlikely).

So, this the perfect vehicle to stash your savings with a highly respectable return.

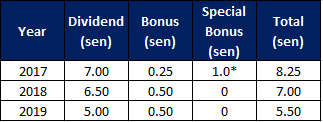

Think of the total dividend (sen) as percentages.

Example

Assuming we had RM100k in my ASB account in 2019.

We’d be entitled to 5.5% dividends or RM5,500 cashed in early January 2020.

Of course, this amount is prorated.

This means that if I put the same RM100k on the 1st of December 2019, I’d only be eligible for 31 days worth of dividends, or RM467.

No, you can’t cheat the system by putting in all your money on the last day of the year (trust us, we tried).

Notice that the dividends have decreased in 2019, due to the Malaysian stock market suffering a bad year, being one of the worst performing markets in the world.

Despite that, ASB and ASM returned a commendable 5.5%, so kudos to them.

All in all, ASB & ASM are great options for those just getting the hang of investing.

The good returns and capital value protection make it a solid, low risk choice for all Malaysians.

We find this to be the perfect tool to stash my savings/rainy day fund since it’s highly liquid (just make a trip to any of the big banks!)

They also have a neat auto-debit feature online to help with our recommendation of “Save first, spend later”.

ASB Financing

Note: This only works for Bumiputeras (sorry guys).

Onto the juicy bit, where the real returns are.

ASB is such a safe investment that banks are willing to loan individuals like you and I up to RM200,000 to invest.

Why would the banks do this?

Banks are in the business of making money.

They charge you interest on the loan, while having close to zero risk.

If they are charging me interest, why should I take a loan? Isn’t it better to invest myself?

The key word here is leverage.

The bank is giving you RM200,000 in capital to earn dividends and in return, you pay instalments of around RM1,050 per month for a loan tenure of 30-35 years (we recommend to always go for the longest tenure).

Example

Assuming ASB announces 7% dividends in 2020.

John has 1,050 per month to invest.

John decides to put this into ASB directly every month.

At the end of 2019, he has RM12,600 in capital (1,050*12) and RM480 in dividends (calculation for this is slightly complex, so I’ll omit) for a total of RM13,080

Jane also has 1,050 per month to invest.

Janes goes for ASB financing instead, taking the RM200k loan.

At the end of 2019, she receives RM14,000 in dividends and has paid off RM2,800 of the RM200k she borrowed (meaning if she terminated the loan, she will receive RM2,800 from the bank as capital paid).

This brings her total to RM16,800, a significant 28% more than John.

Now, 2 factors are incredibly key for ASB financing to work out:

- Bank interest rates

- ASB declared dividend

We suggest choosing the bank with the lowest rates (duh), and only go for it if it’s below 5%.

This should be the case considering BNM’s recent OPR cuts.

In terms of ASB’s declared dividends, this is something we can’t control.

After doing some calculations, we’ve come to the conclusion that ASB financing will only be worse off if ASB dividends go below 5%.

Most noteworthy, 2019 came dangerously close at 5.5%.

For now, we would still recommend pursuing ASB financing until we see 2 consecutive years below 5%.

2 additional perks to ASB Financing

a) You’re obliged to pay the loan installment every month. This is a way to “force” savings.

b) Again, being a loan, this is a great way to start building your credit score with low approval requirements

The first investment I made after starting work was ASB Financing, and I’ve had no regrets so far (fingers crossed!).

Personally, I went for a RM100k loan with a monthly installment of RM529.

However, this is my personal limit, but it would work the same whether you wanted to take on an RM50k or RM200k loan.

I’ll share the agent I used to get this loan to those whom are interested.

We’ll continue this series of giving a detailed description of each investment vehicle and our thoughts on it.

If something you’re interested in isn’t listed, or have more questions regarding this topic, feel free to drop a comment 🙂

Till then!

These articles might interest you:

Your 100k loan is for how many years refinance?

Will you take it out after 5 years similar to many other blogs that I have read?

How much is the interest rate now?

Do you think I should invest in asb financing considering I put 1000 in every month? But I just worried of the credit score only.

Actually I have been hesitating and thinking whether to put it. Anyway it’s a loan and should I just put in 1000 each month or borrow more and pay 1000 to the bank for more dividend ? And follow everyone after 5 years take it out?

The loan duration should take the maximum one ?

Please give your advice?