Table of Contents

Savings vs Investments

Are they the same thing? Think twice.

Many people don’t distinguish between their savings and investments. Anything that you don’t spend and leave in your bank account is good… right?

Wrong.

It’s vital to separate the two. Here, I’ll share my take on how to structure your savings to fully maximize returns, and making the right investments with your excess money.

Savings

Savings represent your rainy day fund. Your f*** it money. Essentially, it’s money that’s easily accessible to you in the event of an emergency.

Good practice is to have between 3-12x your monthly expenses in savings. Yeah, its a large range. Identify the sweet spot depending on how confident you are of securing your next income stream in the event you lose your current one.

Personally, I go for 3x my monthly expenses. This is because I have little to no commitments (remember the benefits of this?). Also, being a fresh grad makes it way easier to get re-hired by another firm.

Important point: Build your savings first before venturing into investments. This was tough for me initially as savings generally have lower returns. I wanted a get rich quick scheme. I compromised and found great avenues to stash my rainy day funds that meet the following criteria:

1) Liquid

We need this money to be available to us quickly since it’s for emergencies

2) Safe

The investment needs to be safe (no fluctuations). Imagine saving 12 months worth of expenses only for it to lose half its value when you need it… yikes

With this in mind, these are the options I came up with:

1) Stash it under your pillow

Yep, nothing can go wrong here… (don’t do this)

2) Bank savings account

Extremely liquid option. Withdraw your money anytime. I recommend putting 25-35% of your savings here for real emergencies that needs money immediately. In general, saving accounts return ~1.5%. Compare this to Malaysia’s inflation rate of 2-3% and you’re actually losing value by keeping your money in the bank.

3) ASB or ASM

Best thing since sliced bread. As mentioned in my previous article, these funds do not decrease in value. Whilst not as liquid as storing in your bank account, a quick trip to any major bank will give access to your funds, which is good enough. Even with a “bad” return of 5.5%, it blows away saving accounts. Recommend putting the 65-75% balance here.

*ASB financing doesn’t fall under this category.

4) Fixed deposits

Next best thing to Amanah Saham. Fixed deposits nowadays are incredibly liquid due to technology and online banking. (Tell your mum she doesn’t actually need a physical certificate anymore). FD’s can be uplifted at any point and while you may lose out on interest, who cares? This are your savings after all. They’re not meant to give you great returns.

Now, you’ve saved up a comfortable amount in your rainy day fund. You’re ready. Time to have some fun with investments.

Investments

Investments are where you let your money grow. Think of it as planting a seed for your future, providing endless supply of avocados in the long term if you nurture it well enough.

You do not want to be pulling your seed out of its roots before it even gets the chance to grow. Same goes here, investments aren’t meant to be withdrawn in the short-term. If you’ll be needing the money soon, it shouldn’t go to an investment.

Why? Investments are volatile and can decrease in value. Imagine putting RM1k today and needing it two weeks later, only to see the value dropped to RM800. Take an L.

Leave the money in there to grow. Deposit monthly, follow the mantra of “Save first, spend later”. Ignore short-term price fluctuations and keep nurturing your avocado plant. One day it’ll pay dividends.

Cool, so where do I put my investments?

I categorize my investments into 2 categories:

i) Safe investments

ii) Riskier investments

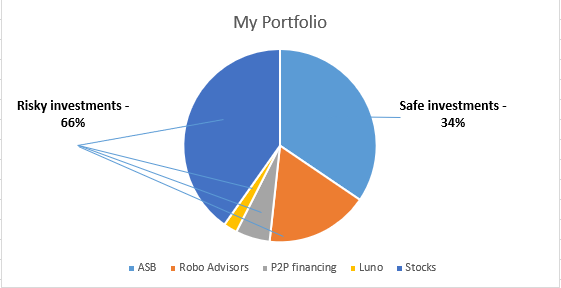

Just because you’ve got your rainy day fund set up doesn’t mean you go absolutely ham with risky investments. A good rule of thumb is to take 100 – your age, and have that in riskier investments. In my case, I should have 77% here (100-23) and the balance in less volatile products.

Why? The younger you are, the more time you have before you need to cash out the money for retirement. So, any short-term volatility such as the 1996 Asian Financial Crisis or the 2008 recession should have little impact on you. Just keep investing.

The idea is to look for riskier investments that give better returns. There’s no point adding risk with no extra benefit. A good benchmark will be ASB. If it doesn’t outperform ASB, don’t bother.

All Malaysian’s get ~22% of their base income in EPF (if you don’t, contact labour law). These are considered safe investments since the fund doesn’t decrease in value. Keep this in mind when allocating your portfolio.

List of “safe” investments:

- ASB (not financing)

- Government Bonds

- Treasury Securities

- Fixed deposits

I’d say nearly everything else is considered a riskier investment. The money you put in the safer investments is so you’ll always have some extra spending money when you need it, preventing the need of dipping into your savings.

Personal

Look, I’m not perfect. The reason I have so much in ASB is because with ~7% returns and close to zero risk, the risk reward ratio was far too good to pass on. With the recent slash in dividends, I’ll be looking out for better places to shift some of this and maintain ~20% in ASB.

This is just an illustration of how you can manage your portfolio and have an idea of how to balance its composition in relation to your age.

Thought it was key for me to differentiate the two before I go further into the different investment products. Next up – Robo advisors!

Till then! 🙂