Table of Contents

12-15 minute read

Are you new to investing and robo advisors? This article might help.

If you’re not new, let’s talk about the 3 robo advisors that you can invest with.

StashAway and Wahed Invest are the 2 most popular robo advisors in the Malaysian market.

The only other player is a Japanese based firm called MyTheo.

I’ve put money in all 3 of these with varying lengths, giving me an idea of what I like and dislike about each of them.

In this review, I won’t be going through MyTheo since I’ve withdrawn my investments from them.

I didn’t really like their portfolio allocation at the time and since I’m unsure if things have changed since then, I’ll omit them for now.

(UPDATE: I have reconsidered this statement and will give MyTheo another go. Portfolio review has been added)

Also, since I (and everyone in Malaysia) haven’t had much time with Wahed Invest, I’m going to focus more on the investing fundamentals and user experience of these robo advisors.

I consider my investment time frame to be way too short to be able to draw conclusions based on the returns.

Let’s get started!

1. StashAway

UPDATE: StashAway has re-optimized their portfolio since this post. You can read our article on the changes here.

Being the first to enter in Malaysia, it’s safe to assume that StashAway holds the biggest market share over here.

StashAway User Experience

Very clean and easy to navigate interface.

All through the StashAway app, I’m able to look into each individual investment and see its composition, performance, and allocation.

Big plus: I also get to start new portfolios with varying risk levels and move funds between them all through the app.

StashAway Performance & Returns

StashAway has big diversification in multiple asset classes.

As mentioned in part 1 of this article, the exposure I get to so many financial assets is huge considering my capital.

I have 2 portfolios with StashAway, being 18% (moderate risk) & 36% (very high risk). Through these, I’m exposed to:

- US Equity Sectors (small cap, healthcare, consumer discretionary, communication, energy, technology)

- Europe equities

- Government bonds (emerging markets & US)

- Corporate bonds

- Gold

I like this split as it gives me good exposure to US & European stocks as well as government/corporate bonds.

These are financial assets that are found nowhere else in my portfolio, which makes them all the more valuable.

In my 1 year with StashAway, they’ve only performed a portfolio re-optimization once.

What this means is they identified a weakness in one of the funds, and switched it out for another.

Previously, StashAway used to include investments in Asian equities.

Instead, StashAway swapped them out for European equities which I honestly prefer myself.

At least it shows their re-optimization claims aren’t just empty words!

Additional note: StashAway investments are denominated in USD instead of MYR, meaning we also get currency diversification!

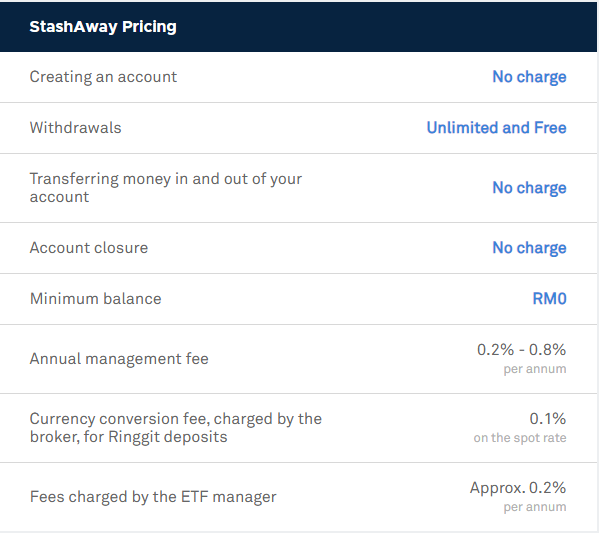

StashAway Fees & Deposits

Great fee structure.

Minimum deposit is RM100 and there are no fees to deposits or withdrawals.

Annual management fee of 0.8% is high for robo advisor standards, but still significantly lower than most mutual funds

StashAway Areas For Improvement

1. StashAway removed weekly deposits! I’m currently on a weekly deposit plan that’s auto deducted from my bank account (forced savings).

Now, StashAway’s lowest frequency deposit is set at monthly… Not a big deal, but still annoying for me

2. Difficult to see performance. StashAway only display returns since inception, it’s difficult for me to go through monthly/quarterly/yearly performances of my fund.

Overall

StashAway is probably still my favourite robo advisor to date.

In 2019, it recorded an 18% return on my investments. Below the S&P 500’s 29%, but more than 3x ASB’s 5.5%.

Check out StashAway’s user reviews on Seedly if you want to know what people think about the investing app.

My investment in StashAway

I put in an initial RM100 in StashAway in December 2018 and set up auto weekly deposits ever since then.

Interested in using StashAway for your own investment? Use this link to get 50% off StashAway’s management fees for 6 months! 🙂

2. Wahed Invest

I’ve just started with Wahed Invest.

Wahed Invest is an online Halal investing robo advisor that’s based in the US. They are the third player to enter the market in November 2019.

Wahed Invest User Experience

Honestly, it’s not that great.

It could be that Wahed Invest is using a different interface than the one they use in the States, but the current one is quite bare bones to me.

Hopefully they touch it up a bit to include more features in the future.

Also, the Wahed Invest web app hasn’t launched in Malaysia.

Not a deal breaker for me, but sometimes I like going on my laptop to go through my investments.

Wahed Invest Performance & Returns

Similar to StashAway, I get good diversification in my Wahed Invest portfolio.

I’ve been allocated to the “Aggressive” portfolio, but I’m looking to move up to “Very Aggressive”.

Funds I’m allocated in:

- US Stocks (Large firms that are Shariah compliant)

- Sukuk

- Malaysian stock (Islamic Dividend Stocks)

- Gold

Overall, a good mix of products.

A bit less diversified than StashAway but you still get a good mix of financial assets in Wahed.

Right off the bat, the main thing I don’t really like is the exposure to the Malaysian stock market.

Yes, it’s good that we invest in our very own companies (Maxis, Petronas, Time) and support them but that’s what ASB & EPF are for.

Through these 2 investments, I already have enough exposure to the Malaysian market.

What I’m looking for is diversity to other regions so I get a good mix in my portfolio.

Still, I’m going to ride this one out for a few months and see how things go.

Big plus: Wahed Invest is a certified Shariah compliant investment. For those seeking investments in only ethical businesses, this is the one to go for.

Wahed Invest Fees & Deposits

Very similar to StashAway, but Wahed is slightly cheaper at low investment amounts.

Minimum deposit is also RM100, which is an affordable amount of money to start off with.

Wahed Invest Areas For Improvement

- Don’t want it to seem that I’m not nationalistic, but I’d like them to slightly diversify away from the Malaysian market. There are so many opportunities out there!

- You can’t have more than one portfolio. On other roboadvisors, you can create as many portfolios as you want and have some range for your investments (High risk vs low risk). On Wahed Invest, you can choose only one, which I hope they change sometime soon.

Overall

I’m going to give Wahed Invest time.

I don’t want to rule out and investment too quickly before having a proper go at it.

For all I know, I could be proven wrong.

I’ll also look past the user experience challenges for now but expect them to make some changes soon.

My investment In Wahed Invest

I just started this year with an RM100 initial deposit in Wahed Invest.

Good thing is I can set a weekly deposit, which I’ll start off with and see how things go!

If you’re interested in opening an account with Wahed Invest, use the code emibin1 so you and I both will get RM20! That’s 40% immediate returns on an RM100 deposit 🙂

3. MyTheo

Finally, we have Japanese based MyTheo!

They were the second player to enter the Malaysian roboadvisor market after StashAway.

The thing that intrigues us the most about MyTheo is their naming.

I have to say.. That’s clever so kudos to MyTheo.

MyTheo User Experience

Very simplistic looking user interface, yet everything that needs to be done can be done.

Like StashAway, MyTheo users can create multiple portfolios if you want to split your money into high risk/low risk buckets.

MyTheo also have a neat “News” section that gives you updates on the market as well as monthly MyTheo Performance Reviews, which is kinda cool.

Having the MyTheo app break down and explain their investments can provide ease of mind for some.

MyTheo Performance & Returns

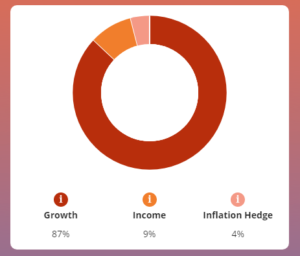

MyTheo has a slightly different way in building your portfolio.

They have 3 main pillars of investments being Growth, Income, and Inflation Hedge.

You get to play around with these allocations to suit your appetite.

The growth section compromises mainly of stocks, income of bonds, and inflation hedge of commodities.

One thing I have to say, MyTheo’s portfolios are incredibly diverse.

And that’s probably understating it.

Going through my portfolio, I counted 26 different ETF’s with a RM100 investment. That wasn’t a typo… 26.

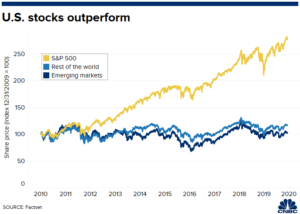

Another distinction with MyTheo is the geography of their investments.

As you can see in my StashAway & Wahed Invest portfolios, they are very heavily weighted towards the US stock market.

MyTheo on the other hand spreads out their investments over multiple countries and only have a small portion of the investment in US based ETF’s.

Now there are some pros and cons to this.

The good thing about MyTheo is we get much better diversity and it’s nice to have exposure to the Indian, Australian, and Singaporean stock market — something I don’t have through any other investments.

These countries could potentially grow quickly which would bring nice returns on our investments.

I still question the big allocation to the Japanese stock market though..

The Nikkei 225 peaked in 1990.

You read that right.

If you invested in the Japanese stock market in then, you’d still be down over 40% – after 30 YEARS.

It is possible that a turnaround happens but decades long stagflation and a decreasing population means Japan is not an ideal place to invest.

Another thing we need to take into account is the fact that over the last 10 years, the US stock market has greatly outperformed the rest of the world.

Global markets had a decade to forget while the US stock market went on its longest ever bull run.

I’m not saying this trend will continue, but it would suck to have your investments under perform by so much over a 10-year period.

Having said this, I don’t mind it at all as I have sufficient exposure to the US stock market through StashAway and Wahed Invest and MyTheo will be a nice diversification tool for me.

MyTheo Fees & Deposits

MyTheo has the highest fee structure of all 3 roboadvisors in Malaysia.

However, the 0.2% difference versus the other two doesn’t faze me too much and it won’t have a significant impact.

MyTheo also have a minimum deposit of RM100, something not practiced by StashAway or Wahed Invest.

MyTheo Areas For Improvement

1. Reduce or explain Japan investment. This might sound extremely harsh, but when ~20% of my investments are in a market that on paper seems unattractive – it just doesn’t sit right. Maybe I’m wrong and Japan is in fact on the road of recovery though. Let’s see.

Overall

I’ll admit this – about one year ago I put in RM100 with MyTheo but after just a month, I decided to withdraw it and close my account.

Looking back at it, I realized I was probably too hasty in making that decision.

I’m giving MyTheo another go and I’ll leave it for the long run.

I like the fact that I’m invested in markets I’m not exposed to elsewhere in my portfolio.

Hopefully it’ll pay off!

If you’d like to invest with MyTheo, you can use think link and get 3 months worth of management fees waived!

Tips to start

I’m gonna try to keep this short & sweet since I’ve gone through this quite a bit!

Here are a few pointers that I can think of:

1. Use Dollar Cost Averaging

Dollar cost averaging is an investment strategy in which an individual places fixed amounts of deposits on a scheduled interval. Essentially, it means setting up a scheduled recurring deposit (weekly/monthly).

I personally use this because it’s a good practice to average out my investments. If you save up your money before depositing a lump sum, you could be unlucky and purchase at a high point in the market.

On the other hand, having small weekly/monthly deposits averages out your buy prices. Sometimes you buy when the market is high, others you buy when its low.

In the long run, things average out.

2. Go for higher risk investments

Now this one is to my younger audience (35 & below).

The younger you are, the more risk you can afford in the financial market. Just remember to only put in money that you won’t be needing in the near term as prices are volatile.

For those who are a bit older, determine the current split of assets in your portfolio.

If you’re quite heavy on safer investments (EPF, ASB), then go for the higher risk portfolios on StashAway/Wahed Invest.

To re-emphasize, these are purely my opinions.

Its always good to start safe and move up once you get more comfortable! 🙂

3. Ignore the fluctuations

I know, I know. I’ve been there too.

Seeing your hard earned cash decreasing in value is a hard pill to swallow.

It takes time to get comfortable with this notion but it’s inevitable that there will be price fluctuations.

Don’t be too hasty in taking action.

Just because your portfolio is down 5% in your first month isn’t a reason to pull out.

Investing is a marathon, not a sprint. Just keep at it.

If you find it hard to sleep at night sweating about this, it’s a good sign that you’re either:

- Taking on a portfolio too risky for your preference

- Putting too much money in

Make the adjustments and gradually increase as you get more comfortable with this.

All in all, I highly recommend robo advisors as part of all portfolios. You can’t really go wrong with either of the 3 choices mentioned in this article.

1. Use our super special StashAway link to get 50% off management fees for 6 months!

2. Use my Wahed Invest code emibin1 so we both get RM40 once you’ve made your deposit!

If you enjoyed reading this article, share it with your friends & family! We’d really appreciate the love & support 🙂

Clear and objective. Hope to see periodical review from you. Thanks

Thanks Beng! Update coming soon 🙂

Really enjoyed this article – comprehensive and clear. Thanks for sharing.

Thank you Aisha!

Thank you for the great insights 🙂

No problem, hope it helped!