Table of Contents

Retirement seems so far away for me. Being in my early 20s, I have ~40 years till I reach the standard retirement age of 65. Who needs to start planning their retirement savings now right? Apparently, me…

I have a fear of reaching my golden years and still having to break my back to earn a living. Much respect to those who are doing this, but it’s just not something I look forward to.

I want to be financially free. Don’t we all? Unlike many others, my aim isn’t so I can stop working and be able to travel around the world for 30 years. That’s not for me. I want it because having financial freedom allows me the flexibility of choosing what I want to do.

I don’t despise going to work, I actually enjoy working on things I’m passionate about. Yeah I can save up a lot now and try to retire early, but I also love enjoying the finer (and pricier) things in life!

So retirement to me isn’t when I’m 60 and finally call it a day, it’s when I have solid retirement savings and can stop focusing so much on doing whatever it takes to make money. After this point, a burden will be lifted and I’ll be able to explore the 200 ideas I’ve come up with sitting at my desk job. If these two things come hand in hand, then all the better!

Now I know not everyone is like me, and that’s completely fine. However, we can easily draw out our financial goals the same way so we can achieve what we want when we finally retire.

So when should I start saving?

A lot of people have this mindset that it’s so far away, I can always start my retirement savings later on in life when I’m earning more right? According to reports by EPF, more than 2/3 (68%) of their members aged 54 have balances below RM50k! That’s barely enough to survive past 4 years at poverty wages.

Based on a survey by HSBC, the best financial advice 63% of Malaysian retirees have received is “Start saving at an early age”. The best time to start saving for retirement is when you get your first job. The second best time? Now.

Whilst it’s true that you can save more when you earn more, it’s always good to start early for 2 simple reasons:

1. Creating the habit

Starting to save and invest is a habit. Stashing away 5-20% of your income early on builds the foundation that will make it easy for you in the future. It’s a disciplined process that I’ve instilled in myself so it wouldn’t be any different to me whether I’m earning RM3k a month or RM20k a month.

To add on to this, I’m already exposing myself to the various investment products available in the market at a young age. With experience, I get more and more familiar with what works for me and what doesn’t. By the time I hit my 30’s and my income really starts to hit big (hopefully), I’ll make much fewer financial mistakes since I’ve made them all in my 20’s investing pennies! You don’t wanna mess with your retirement savings, trust me.

2. Compound interest

Widely known in the financial field as the eighth wonder of the world. In a nutshell, it’s when your money starts making money for you.

Illustration

I invest RM100 in my first year with 6% returns. In total, I make RM6 and bring my account up to RM106. In my second year, I make 6% returns on my RM106. This time, I make RM6.36, bringing my account to RM112.36. This scales much more as the value and time horizon increases.

If you invested RM100 once in a portfolio that yielded 6% returns annually, you’d see a gain of RM79 in your first 10 years. Not bad, but nothing special. In the following 10 years, your portfolio goes up by RM142, nearly double the first 10 years. In the final 10 years, it goes by a significant RM455. More than 5x the first year’s return.

When looking at it like this, every RM100 you spend now is technically RM1,029 you could’ve spent in your 60s/70s. That’s the power of compound interest. The earlier you start, the bigger returns you see in the future.

How much should I start saving then?

This depends on your goal. A few key factors that influence this:

a) How much do you want for retirement?

b) How many years do you have to retire?

c) What’s your starting capital?

How much do I need in retirement savings?

Ignoring inflation, think about how much you want to spend a month. Let’s assume this amount is RM5k. Annually, it comes up to RM60k. A good way to measure how large of a nest egg you need is using the 4% rule.

Take your annual expenditure of RM60k and divide it by 4%, bringing your capital requirement to RM1.5m. That’s a LOT of money. This ensures your returns of 4% annually is sufficient to continue your lifestyle, maintaining your hard earned savings.

Technically, you don’t need that much. Spending RM60k a month, drawing down from a portfolio of RM1m would last you ~17 years. The only thing is.. you’d have no money after. For each their own!

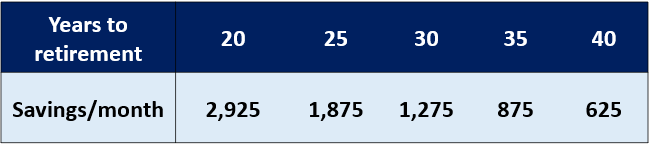

“Ok fine, how do I get to that 1.5m mark?” It depends on how many years you have till retirement.

If you put this into perspective, it’s a very achievable amount to save monthly. Don’t forget that Malaysia’s mandatory EPF means you’re forced to save ~23% of your monthly pay, which should help you get to the amount. However, it’ll only work if you manage to leave your EPF untouched till you retire.

This also reiterates how important it is to start early. If you have 40 years to gather the RM1.5m, you only contribute a total of RM300k, with the further RM1.2m coming from investment returns. If you have 20 years, you’ll be putting in more than double the amount at RM700k, with “only” RM800k in returns.

My strategy

As I mentioned earlier in this post, my idea of retirement isn’t when I completely stop working. It’s when I have enough in retirement savings that I no longer have to put financial gains as my priority when choosing a job.

I’ve figured that by not touching my EPF, I’ll have a nice sum to retire with once I’m able to withdraw it (55-60 years old). So, the focus now will be on building my nest egg for semi retirement.

Since I haven’t quite yet decided when this will be, I’ll continue doing what I do and re-evaluate my progress every year. Currently, the important steps I’d be taking would be:

a) Focus on growing my income

b) Saving and investing much as I can

I’ll continue with my monthly investments and increase this as my compensation starts to go up. Since I’m young, I’ll be going for higher risk portfolios with higher potential returns, something I recommend my fellow millennials to adopt.

See the 3 reasons I use robo advisors

And ASB Financing – a worthy investment

Again, I’m not too fussed about giving up all the good things in life so I can retire at 35. I’ll always manage how much I spend but it’s important to stop and smell the roses along the way.

“I found out retirement means playing golf, or I don’t know what the hell it means. But to me, retirement means doing what you have fun doing.”

Do you feel like you’re on the right track? Leave a comment on what your retirement strategy is and we’ll be happy to have a chat!

Very good la you. Need more advice like this

Appreciate the support man!